|

Disability income insurance from an employer-paid, group plan offers the advantages of basic disability coverage at minimal cost to you as an employee. However, these plans have their limitations, and knowing what they do and don't cover is a critical part of your planning process. Here are the most common aspects of a group long term disability plan I go over with clients:

|

|

1). Own-occupation Definition: How the policy defines disability is of paramount importance (I explain the importance of own-occupation definitions in this blog). Usually I see group policies only give the employee "own-occupation" definitions for the first 2 years of claim. After 2 years, the definition changes to "any-occupation" to age 65 (or whatever the benefit period is set at). The plan may not have "own-occupation" definitions at all, but simply "any-occupation" definitions. We don't know until we look through the policy. Do you know what you have?

2). Mental/Nervous Coverage: Group plans typically limit disability benefits to only 2 years if the disability is mental/nervous in nature. The plan could completely exclude claims pertaining to mental/nervous disability. This is a big deal and you need to be aware of what you have (I've written on mental/nervous on a previous blog). If you cannot work due to depression, anxiety, or substance abuse and your group plan only offer 2-years of benefits, you need to anticipate this in your financial planning.

3). Benefit Amount: Your run-of-the-mill group long term disability insurance policy covers 60% of salary. I've seen it as high as 66% and 70% of salary and as low as 40% of monthly salary. I've seen a plan that insured 60% of salary for 2 years of disability and then dropped the coverage to only 40% of salary for the duration of the claim after the 2-year point. If your employer is paying all or most of the premiums, your benefit will likely be taxable. If your group policy covers 60% of your salary, how do you feel about taking a 40% pay cut when you're disabled? See more of my comments on monthly benefit here.

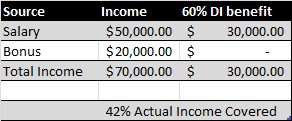

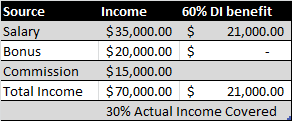

4). Income Insured: Your typical group plan only insures salaried income only, not usually income from commissions or bonuses. I occasionally see commission income covered and even less frequently bonuses insured. If you derive a significant portion of your income from bonus or commission and your group disability plan offers you 60% of salary covered, you may not be getting 60% of your income insured. For example:

5). Cap: No matter how big your salary is and what percentage of it your group policy will insure, there's a benefit cap in place. It's typically $5,000 of monthly benefit. Could be higher, could be lower. I know one hospital system that has a cap at $23,000/month and a hospital residency program with a cap of only $3,000/month. If your group plan caps at $5,000/monthly benefit and insures 60% of salary, the minute you make more than $100,000 in salary, the cap works against you. Here's how it would pay out: $70,000 salary x 60% = $42,000 = $3,500 of monthly income $100,000 salary x 60% = $60,000 = $5,000 of monthly income $120,000 salary x 60% = $72,000 = $5,000 of monthly income (not $6,000/month like you'd want)

6). Benefit Period: Typically, these plans give a benefit period of to-age-65, but don't assume. I've seen some that give a benefit period no longer than your years of employment with the company if you've been employed for under 10 years. In this scenario, if you've been with the company only 3 years, and become disabled, you're only getting disability benefits for 3 years. Not familiar with a benefit period? I walk through them on this previous blog.

|